Many people know what credit they have - whether it's good or maybe a bit more "colorful", but most of us don't actually know what makes up our credit score. Start by accessing your full credit report at www.annualcreditreport.com. You can also use apps like Credit Karma or Credit Sesame to monitor your progress.

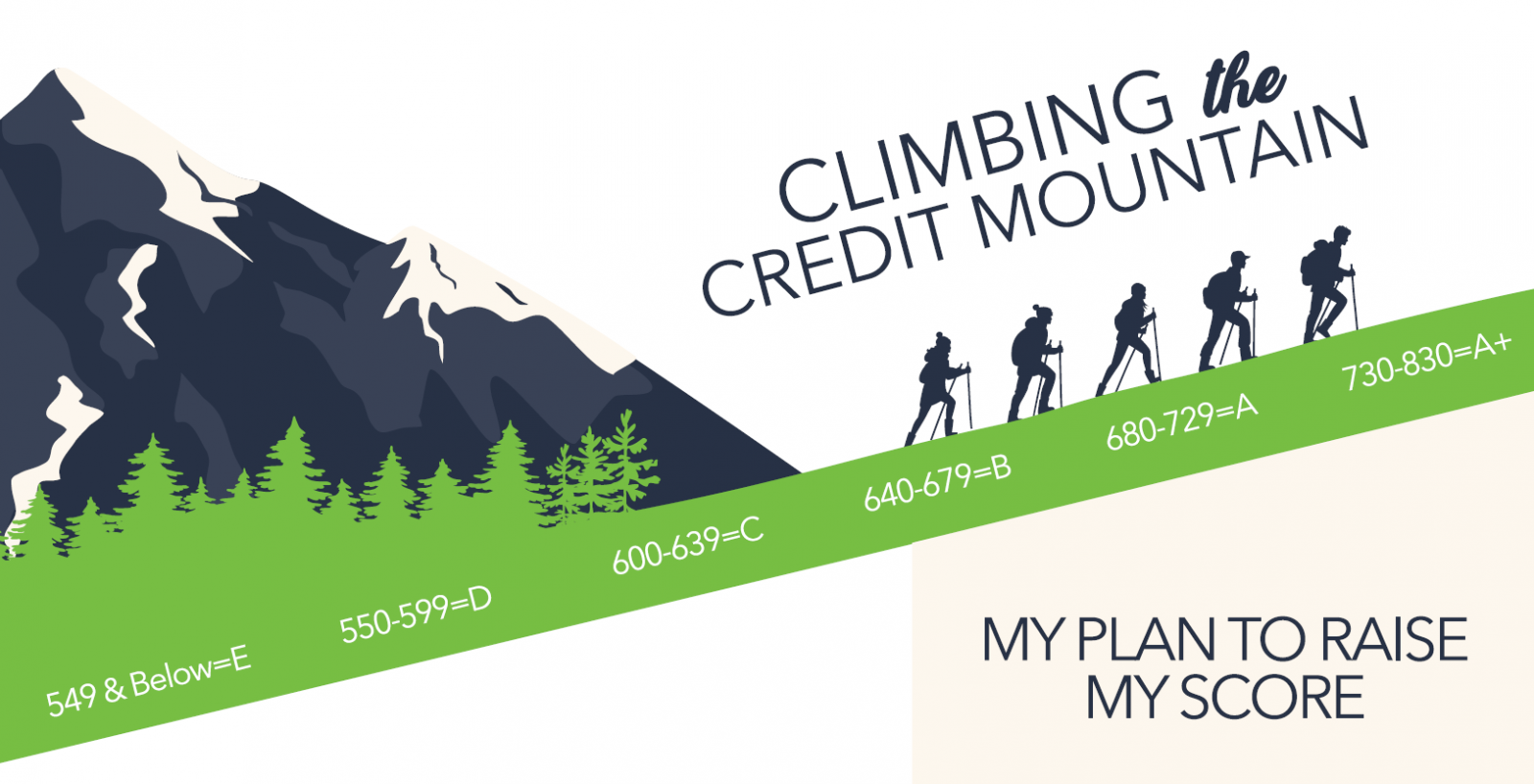

No matter what your credit score currently is, you can always improve this score! By knowing exactly what affects your credit score (and how much), you can start your climb up the credit mountain and we're here to help every step of the way.

So what makes up your credit score?

- 35% = Payment history (i.e. on-time payments or delinquencies)

- 30% = Amount owed (a.k.a Capacity)

- Think of capacity as a ratio between what you owe and your available credit (amount owed: available credit = your capacity)

- 15% = Length of credit

- 10% = New credit (accumulation of debt in the last 12-18 months including number of inquiries and opening dates)

- 10% = Type of credit

- Installment debt - a set loan amount that you pay back in steady amounts every month like car loans, mortgages, etc.

- Revolving debt - loans where you make charges, pay them back and can make more charges like credit cards, lines of credit, etc.

What actions hurt your score?

- Missing payments - affects scores 60-100 points

- Credit cards capacity (how much you owe) - approximately 1 point for every % used

- Shopping for credit excessively - plan for no more than 2-4 inquiries per year

- Opening up numerous trades in a short time frame - recommend no more than 2-3 accounts per year

- Having more revolving debts in relation to installation debts (see above for definition of installment vs. revolving)

- Closing credit cards out (this could lower your capacity)

- Borrowing from finance companies

- See your credit union first! We're here to help.

How can you improve your score?

- Pay off or pay down on your credit cards

- We recommend not closing credit cards as it may decrease capacity

- Exception: when you have had a bad experience with credit cards and don't want to go down that road again or are paying an annual fee

- Move your revolving debt to installment debt

- Continue to make payments on time (older late pays will become less significant with time)

- Slow down on opening new accounts

- Acquire a solid credit history with years of experience

So what's your next step?

If you have more questions after reading this and want to discuss where you're at, meet with one of our Certified Financial Coaches for free! We'll evaluate your financial picture and discuss a plan of action to help raise or maintain your credit score.